‘Many experts comment on housing affordability, but it is often limited to the generalisation that affordability is at historic lows or, even worse, housing is unaffordable. So, people stop buying – they still won’t succeed. In fact, the matter is a little more complicated and it is necessary to explain it to buyers looking for a home,’ explains Eglė Savostė, Senior Analyst at Citus, a company of creative real estate projects’ development and placemaking.

She emphases that affordability can be better or worse, but Lithuania is still far from a situation where it would be impossible to afford a home. There are certain groups of people for whom housing is less affordable and others who may need to revise their expectations at this point. Still, housing should be considered affordable as long as middle-income earners can afford a home that meets their needs.

‘In principle, there are only two housing affordability indices in Lithuania. One is formed by Swedbank, and the other is by the Bank of Lithuania. Both are based on different calculation methodologies. The first one is slightly more understandable and actively communicated but has drawbacks. The second one is based on a rather complex assumption and does not seem user-friendly for buyers. Therefore, our team has analysed the data and developed the Citus Housing Affordability Index, which covers the affordability of new housing in three major Lithuanian cities and is based on today’s current trends,’ says Eglė Savostė.

Susiję straipsniai

Affordability assumptions are key

The Citus team of analysts, looking at the two existing affordability indices and the available data, noticed that some of the assumptions used in them do not correspond to the current situation. For example, the income of a household of two people should be measured as 1.9 times the average national salary (VDU), and not 1.5 as, according to the statistics of the State Data Agency of Lithuania, the wages of women and wages of men differ much less in Lithuania.

It is also essential to correctly assess what criteria are included in the affordability assessment. The average housing size is often used, but this is not an intuitive definition. Therefore, the Citus team did not take the average housing size as a basis but calculated how many square metres are affordable at current prices. Based on this figure, it is clear that a multi-room dwelling can work out.

Among other less essential aspects, the price detail is also important: it includes not only the price of the house but also the price of the loan, as more homes on the primary market are bought with loans. According to the Bank of Lithuania’s responsible lending policy, the monthly loan payment cannot exceed 40%, which is why this amount was assessed.

Thus, the Citus affordability index shows how many square metres of housing a household can buy on the primary market with a 30-year mortgage loan of 85% of the value of the house and a monthly down payment of 40% of the buyers’ monthly income (after taxes). The banks’ interest margin is treated as a constant at 2%, as it is relatively stable, plus the six-month Euribor rate, which is usually fixed when financing a house purchase.

Statistics on average income are taken from the State Social Insurance Fund’s (‘Sodra’) database separately for each city. The housing price is also assessed based on the average cost of the primary market housing supply in each city as monitored by Citus. This data is planned to be updated every quarter, thus avoiding statistical errors, and published alongside the market overviews.

The affordability of new housing is better than depicted

According to Swedbank’s affordability index and a published survey, housing in Vilnius is no longer affordable. Is this true?

Citus’s senior analyst explains: ‘The situation is not good or encouraging, but at the moment housing in Vilnius is still affordable. Even in the current circumstances, at least people on average monthly incomes can afford housing. And we are talking about new residential property. We estimate that the area of affordable housing for two people together in the last quarter of last year was 55.18 sqm; that is, in terms of average price. People on average incomes will not necessarily buy at the average market price: in locations further away from the centre in quieter neighbourhoods, prices may be lower; therefore, the affordable area will be increased. In foreign capitals, the situation is much worse’.

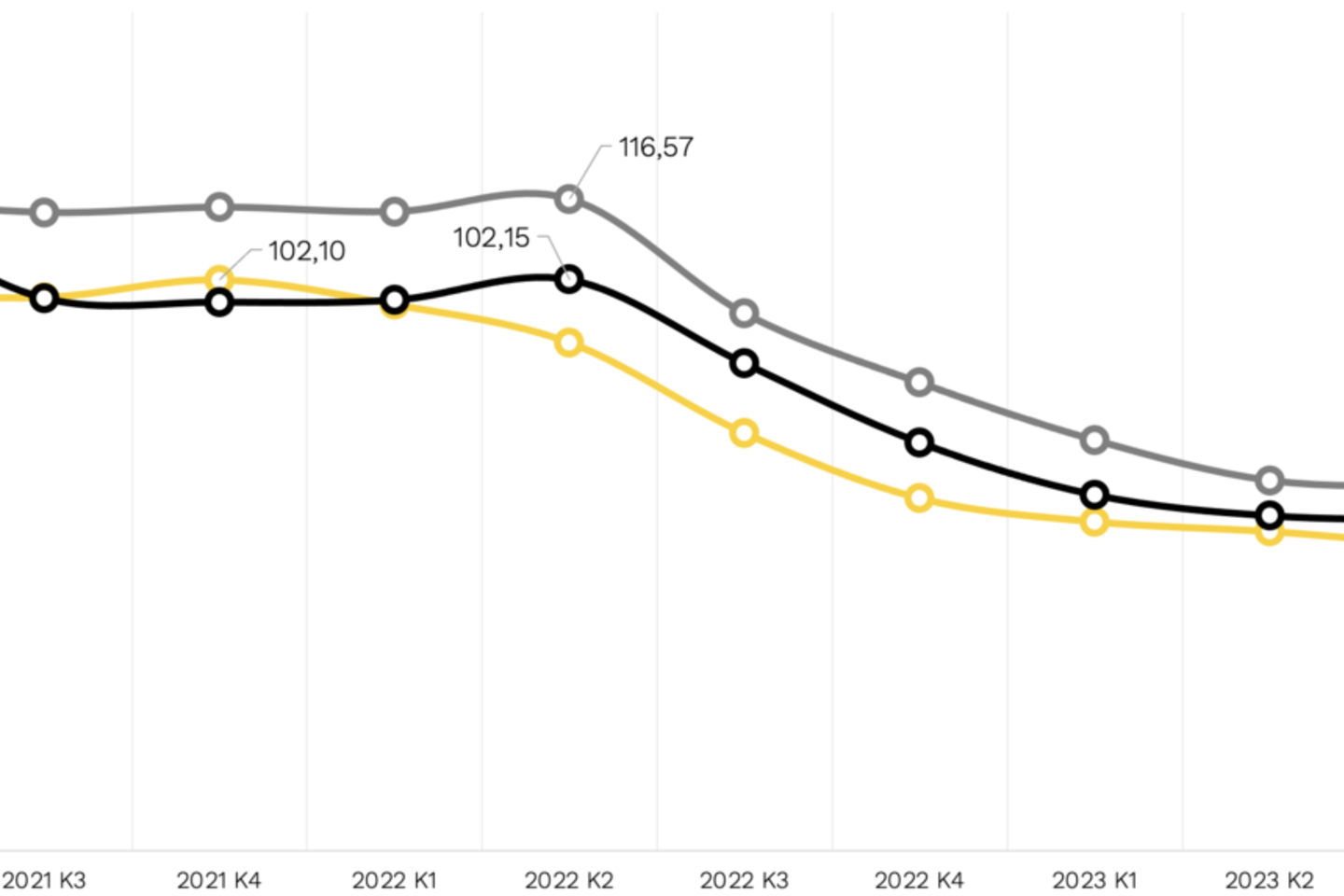

According to her, in Kaunas in Q3 2023, two co-owners could buy a property with an area of almost 61 sqm, while in Klaipėda, this was as much as 66 sqm.

In addition, Eglė Savostė notes that the cost of renting a similar property can be comparable to a monthly mortgage payment. However, the rent is not regulated by the State, unlike the limit on the proportion of monthly income that can be covered by a loan payment. It is, therefore, worth comparing these rates to see whether it makes more sense to rent or own a home.

Chart 1: Dynamics of housing affordability in Vilnius, 2017:Q1–2023:Q4 (Citus data)

Affordability is not only affected by housing prices

Another fact that has been ignored in the affordability debate is the cost of borrowing. It has often been argued that affordability is eroded by rising (or high) housing prices and the expectation that developers should reduce them because of prolonged slack demand.

Eglė Savostė: ‘However, prices in the primary housing market in Vilnius have been stable for about 20 months, and there is no room to reduce them due to the 34.2% increase in construction costs over the last three to four years (according to the Construction Cost Index published by the State Data Agency). Meanwhile, affordability has fallen the most due to the rising Euribor and the unreduced bank interest margins. Comparisons with foreign countries where buyers supposedly are not charged interest have been attempted, but this turned out to be a myth. However, in other European countries, such as Scandinavia, where originate the banks that occupy almost the entire Lithuanian market, the interest margins on housing loans are much lower’.

For example, in the last quarter of 2021, when demand for housing was exceptionally high, and prices also peaked, housing affordability was at its highest level since the beginning of 2017, at 102.1 sqm (Q4 2017.01 – 85.84 sqm). This was due to the strong wage growth not outpaced by house price growth. However, it started to fall when Euribor began to rise and bottomed out with its peak in the second half of last year.

From its peak in September, the six-month Euribor base rate of 4.143 points fell to 3.873% at the end of January. Commercial banks have already started to cut interest rates on housing loans, suggesting that we have already rebounded from the bottom of housing affordability. This is a positive sign for buyers.

For example, if the impact of Euribor alone is eliminated (assuming it is zero), housing affordability for two people in Vilnius at the end of 2023 would have been as high as 89.37 sqm and would be higher than in 2017 when Euribor rate was negative.

Chart 2: Affordability in Vilnius, Kaunas and Klaipėda 2021: Q1–2023: Q4 (Citus data)

Bank competition has increased as the number of home loan customers has decreased. This is because the activity cycles of developers and banks overlap within the period of development of a project. While buyers enter into preliminary deals with developers at the beginning of the project construction, they turn to banks for a loan once the project has reached the required completion stage before notarial transactions. As a result, banks are now starting to feel the drop in customer flow that developers felt as early as 2022, and this year, we are already seeing a drop in bank mortgage margins to 1.5%–1.6%.

Affordability calculations – more perspectives

When calculating the affordability index, Citus analysts also considered other assumptions, such as how many square metres of housing can be afforded by a single person who buys a home with a loan.

In Vilnius, a single buyer can buy a 29.04 sqm home; in Kaunas this is about 32 sqm and in Klaipėda, around 34.68 sqm. This is the size of 1–1.5-room flats, while a 35 sqm flat can accommodate two rooms.

The housing size is decreasing, so the relative affordability remains

Another trend is also evident. Over the last 10–15 years, the area of housing purchased has been gradually decreasing. On the one hand, this is because the price is rising. However, as people start to move to a new home more often (in Lithuania, on average, every seven to eight years), they buy according to their needs and not for life. Therefore, efforts are made only to buy surplus square metres that will be used up. In addition, new dwellings are being designed with increasingly efficient layouts and the available space is being allocated more rationally.

‘By comparison, if a Soviet-built apartment of 30–40 sqm, which is several decades old, is nicknamed a pocket by many residents because of its inefficient design; a new apartment of the same size is enough for most people. Because of the shape of the rooms and hallways, an efficiently designed two-room apartment can be more comfortable than a larger but less well-designed three-room apartment,’ says Citus senior analyst.

In the near future, affordability should improve

Economists are optimistic about the outlook for the Lithuanian economy this year, which is encouraging. According to the Ministry of Finance, whose forecasts are more moderate than those of the Bank of Lithuania, they foresee an annual GDP growth of 1.7%, a 7.6% increase in the average gross wage rate (AWR), and no increase in unemployment. It is not particularly encouraging that most of the wage growth will be driven by increases in the minimum monthly wage and the non-taxable income rate, which will have little impact on those currently in a position to buy a home. Real AWR growth is likely to be lower for potential homebuyers due to the economic slowdown.

In the global uncertainty, we seem to be moving towards a soft landing, so if inflation can be contained as planned, with wages rising and the Euribor rate falling, affordability will also improve.

According to today’s forecasts by Citus analysts, the European Central Bank may start to cut interest rates more rapidly in the coming months, and Euribor could fall to 3.05% by the middle of this year. Real wages are unlikely to change significantly, but housing prices will also likely remain the same. In this case, the reduction in the Euribor alone could increase the affordability of a two-person home with a loan to 61.18 sqm in Vilnius, 67.37 sqm in Kaunas and 73.07 sqm in Klaipėda.

Chart 3: Dynamics of housing affordability in Vilnius, Kaunas and Klaipėda, and forecast for 2024 Q2 (Citus data)

Eglė Savostė explains further: ‘But in the long term, affordability unfortunately tends to deteriorate. This is especially true in capital cities. As the economy grows, living conditions become more comfortable, and as cities become more populated, housing becomes more expensive. Vilnius, Kaunas or Klaipėda are not made of rubber: as cities get denser, the supply of plots decreases, making them more expensive; housing requirements and buyers’ expectations increase, and construction becomes more expensive. While affordability may temporarily improve as wages rise faster, other conditions may change, making homeownership more problematic. It is enough to look at the capitals of other European countries to understand the direction we are moving in and where we might find ourselves in five, ten, or fifteen years," explains the expert.

For example, affordability is around 10% worse in Warsaw, 40% worse in London and 80% worse in Frankfurt.