When buying a home for yourself, the decision becomes very personal. It’s not just about calculating returns or predicting market cycles – it’s about how you feel about the place every day. It’s a decision about your quality of life: peace of mind, comfort and emotional security.

Around 60% of homebuyers in Lithuania purchase a property with a loan. Financing is, therefore, a crucial first aspect. Interest rates have a significant impact on affordability. For example, at an annual interest rate of 3.8%, a monthly payment of EUR 900 makes it possible to buy a home for around EUR 230,000. However, at 5.8%, the affordability drops to around EUR 180,000, a difference that can affect not only the size of the flat but also the choice of neighbourhood.

For this calculation, we estimate that the bank’s interest rate is approximately 1.5%, with the remainder being the 6-month Euribor rate, which is currently around 2.15%, following the European Central Bank’s latest base rate cut.

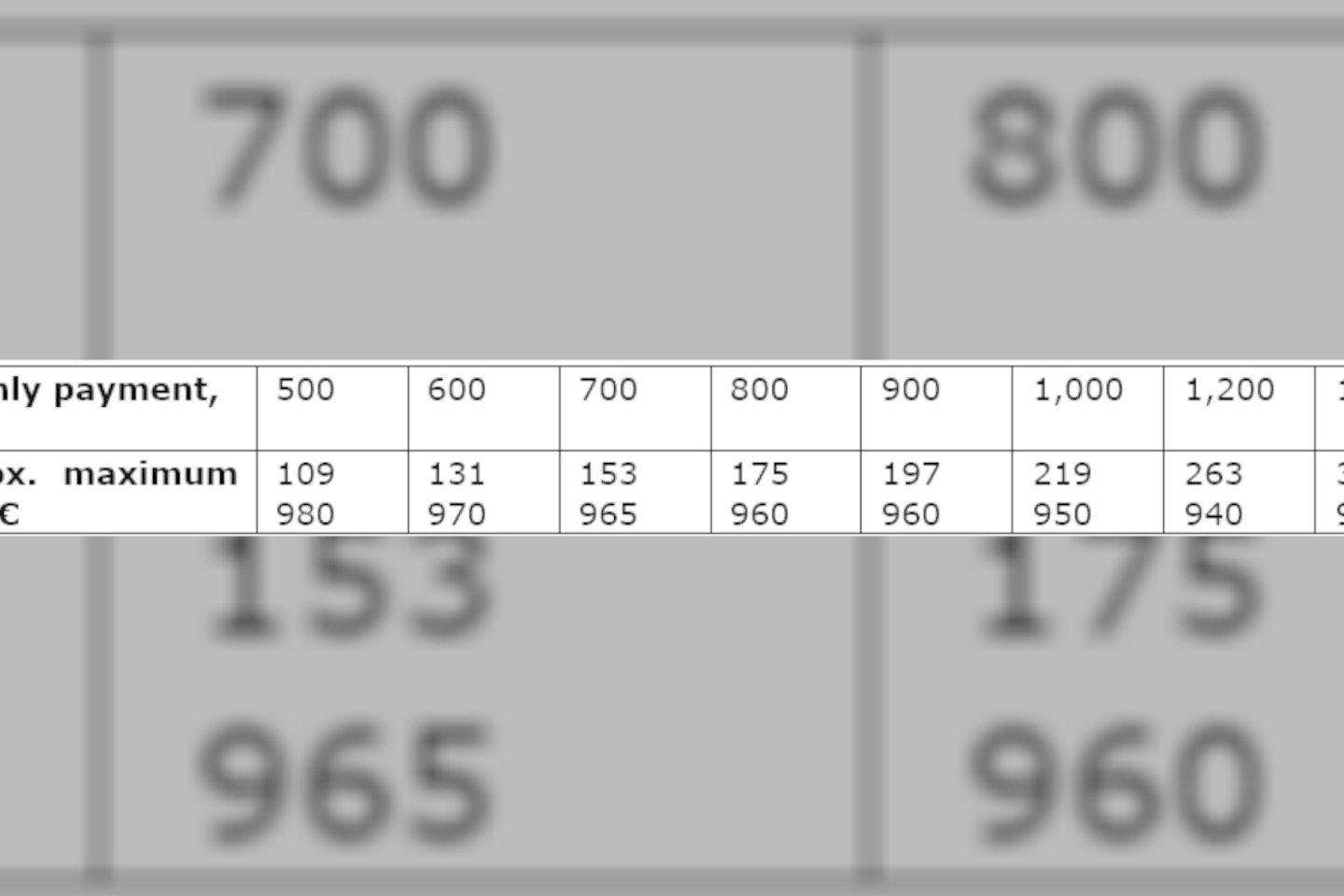

The Bank of Lithuania’s Regulations on Responsible Lending state that financial liabilities cannot exceed 40% of a person’s monthly income. To find out the maximum amount you can spend on loan repayments, multiply your monthly income by 0.4. For example, if the family income is EUR 2,000, the maximum monthly repayment would be EUR 800. You can then calculate how much you can borrow.

Here are the approximate loan amounts by monthly payment:

At least a rough estimate of the loan ceiling allows to reduce the number of options that can be safely purchased within the limits of responsible borrowing.

Additionally, in cases where a second family home is being purchased (after the first one has already been acquired), banks often require a 30% down payment rather than the standard 15%.

Suppose you plan to buy a new home after selling your current one. In that case, it is essential to conduct a thorough analysis, assessing the property’s value, the outstanding loan, personal income tax (PIT) aspects and the terms of the new loan.

If there is a profit on the sale of the home, it may be subject to a 15% PIT if the property is sold less than ten years after purchase. However, the tax does not apply if a new home is purchased within a year of the sale and is the family’s primary residence.

Often, we want everything at once – a bigger flat, an extra room, maybe a place for ‘when I have kids’ or ‘when I work from home’. But it’s worth asking yourself: do I need it now? On average, people move into a new house every seven years. So, it is a more solid decision to choose a smaller yet high-quality home that suits the current stage of life and then move up to a bigger house as a natural progression.

When analysed over a more extended period, the value of housing as an asset tends to increase; for example, a two-room flat worth around EUR 160,000 today could increase to EUR 210,000 in seven years. In this case, replacing a home becomes a logical progression, allowing for a gradual accumulation of capital. Two-room flats are the most sought after on the market at the moment, so their price tends to rise the fastest.

New-build housing is often an attractive option for several reasons. Firstly, they offer lower maintenance costs and higher levels of comfort thanks to modern construction methods. Such housing tends to retain its value and exhibit rapid value growth, especially with well-developed infrastructure and strong demand potential. In contrast, older housing – although cheaper – often requires more investment in renovation and upgrading. However, if the investment is made strategically, purchasing a home in a well-developed area with growth potential can turn an older home into a profitable investment. However, new housing is a more reliable option for those seeking stability, lower maintenance costs and more liquidity.

Choosing a home for yourself is not just about the numbers but also about how it feels every day. Do you feel like cooking dinner while watching the sunset in the evening? Is the kindergarten within walking distance? Is there a green space for walking? Such details determine whether the new home will become a place where you truly feel at home.

More information:

Rytas Stalnionis

Communications Manager

Tel.: +370 614 01829

Email: rytas.stalnionis@citus.lt

www.citus.lt